The customer experience at the world’s biggest banks and fintech firms is undergoing a significant change. Because of technological advancements, account users may now not only transfer money online but also log in using Identity Verification using face match technology and do a variety of operations using simply their smartphone and its front camera. Technology in this area has made things faster, easier, and safer during the last decade.

Customers who are increasingly technologically savvy have grown to demand financial services when and when they want them.

We may even speculate that as youngsters become adults, they will not need to visit a bank in a traditional way because all money management would be done online. So, why has the user experience in many circumstances continued to fall short of expectations? We investigate the answer to this issue and provide methods that both FinTechs and banks may take to enhance their Digital onboarding processes and, as a result, keep their clients.

What is Client onboarding in Finance & Banking?

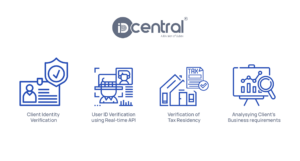

Onboarding is an essential aspect of the process of combating money laundering and terrorism funding, and it is a critical component in the implementation of financial security measures. At a base level, secure client onboarding consists of the following components:

- Client Identity Verification

- Identification of recipient through Document or ID verification

- Verification of tax residency

- Determine the intent of the client’s business.

The extent of the above-mentioned client screening techniques employed is determined by the risk that he or she poses.

Why is Client Onboarding different for distinct types of clients?

The process of onboarding differs based on the type of client. This method differs for an individual and a business (except for sole traders where the real beneficiary is simply the owner of the company). Additional documentation and information are normally not required for retail customers.

The problem grows more complicated for private banking customers, where the number of transactions and the evolution of financial instruments are considerably larger, making the procedure more difficult. Onboarding also differs according to the client’s legal status, which may necessitate the submission of extra paperwork. Even the procedure of choosing the beneficiary will be different in this case – the amount of intricacy may change.

Regulatory KYC & AML screening in Financial Institutions(FI)

Anti-money laundering (AML) & Know your customer (KYC) are well-known and often used phrases in the banking industry. But how do they interact with one another, and what are their differences?

What is Knowing your customer (KYC)

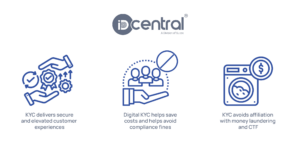

KYC, or ‘Know Your Customer,’ is a basic business procedure for financial organisations worldwide. In a word, it is the process of determining who your clients are, determining if the sources of their cash are genuine, and determining whether they are legitimate users of the platform that they are attempting to access. Obtaining extensive client information protects both sides in a commercial transaction and relationship. As a result, KYC serves several functions:

- It delivers excellent service.

- It avoids responsibility.

- It avoids affiliation with money laundering and other illegal financial transactions.

To summarise, KYC is simply the process of verifying that the client is who he or she claims to be.

What is Anti-money laundering (AML)

KYC is merely one component of AML, which refers to procedures implemented by financial institutions and governments to prevent and combat financial crimes such as terrorist funding and money laundering.

The AML policy of a bank or fintech business is part of a larger AML compliance programme that should be developed in accordance with local AML regulations.

Because the border between KYC and AML practises is blurred, it is even more necessary to have these processes effectively managed, with distinct responsibilities established and tools to aid in coordinating these activities. It’s a high-stakes game that can result in sanctions from authorities.

Understand Anti-money laundering & counter-Financing Terrorism (CFT)

Combating money laundering and terrorist funding benefits global security, financial system integrity, and long-term prosperity. As terrorists and their sympathisers continuously vary their methods of collecting, moving, and gaining access to funds, banks and FinTech institutions must adjust their instruments and policies to deny them the opportunity to participate in illegal behaviour.

How Fintechs can stay compliant with KYC regulations

Risk statuses: Regulators presently demand risk statuses be determined using predetermined algorithms rather than discretionary ways when it comes to KYC. These are frequently dependent on a variety of characteristics, such as the customer’s nation of origin, the intended transactions, their currency, volume, items or services sold, or financial solutions the client would employ.

Based on this information, a decision is made regarding how frequently and how the client should be watched. It is possible that law enforcement authorities become interested in the client throughout the course of the client relationship, which is a direct justification for increasing the customer’s risk class and taking relevant actions against the financial institution. In most circumstances, retail consumers are believed to be low risk, while private clients must be properly scrutinised.

The dependability and speed of operation of such a system are so critical that alarms are generated and actions are validated by (in the Polish case) the General Inspector of Financial Information, the prosecutor’s office, and other authorised agencies. Financial institutions suffer penalties and legal punishments in the absence of an effective consumer control system and its execution. Onboarding is often implemented at the level of a group of financial institutions, however, transaction monitoring may be a local solution because all scenarios demanded by local institutions must be considered.

How to perform Customer Due Diligence

The difficulty in monitoring is maintaining current client data as part of KYC and behavioural tracking. Customers are profiled by financial organisations using Customer Due Diligence (CDD), which determines their transaction profile. This allows them to determine if the customers are functioning within the established profile, which is mostly based on transaction criteria. If these criteria are surpassed, they are recorded in registers as requiring action and are sent to the appropriate institutions.

Most businesspeople have come across a transaction barrier of 15000 USD, over which all transactions must be reported to some government entity. The frequency of transactions is also examined, including whether they originate from and go to specific nations. For example, if a client says he will open one transaction with China once every three months but in reality opens 10 letters of credit with Saudi Arabia on a quarterly basis, an alert should be generated in the information systems about the client’s profile not matching the operations carried out.

How Transaction Monitoring & Screening works

Setting the aforementioned settings has an influence on how many alerts are generated, which in turn has an impact on how many experts need to be engaged to handle this data and customers. The difficulty here is that it is a tough process to automate, because, contrary to the definition of sanction lists, it is impossible to develop algorithms that should monitor the client and his behaviour.

The effectiveness of such a system is critical. A slow reply may result in a situation in which it is impossible to stop the flow of proceeds from the crime due to the amount of time it takes for information to circulate. This might lead to harsh fines. The final step in this sanctions monitoring is to either close the alert, e.g. with the status false positive, or to report the client to law enforcement agencies.

Without such processes, you cannot, for example, acquire a licence to create a new firm in the financial market. Mechanisms of this sort must be built in such a way that responsibility for work done on them and actions taken can be identified.

What are the Onboarding challenges that Banks & FinTechs face

The three key pain points for banks and FinTechs when developing an effective digital client onboarding programme are discussed below:

The difficulty of recognising consumers

Identifying consumers for banking services is a delicate undertaking that necessitates careful consideration of all legal requirements as well as how this new procedure will fit into your existing system.

By using modular tools for authentication flow creation and auto-branding, as well as simple plug-and-play integrations, a comprehensive Identity Verification process can be quickly designed and implemented to capture customers’ data, verify it, and painlessly pass the results back to the bank’s database.

According to research, client onboarding time grew by 18% in 2017 and showed considerable evidence of continuing along this trajectory.

A terrible customer experience

According to the same study, it takes a bank an average of 24 days to complete the customer onboarding procedure, and 89% of clients experienced a negative KYC experience. As a result, at least 13% of respondents switched to another service provider.

There has long been a widespread assumption that increasing security must come at the price of consumer delight. That is, when security measures improve, there is more inspection, which generates more friction for the consumer and, as a result, a negative impact on the entire customer experience. This idea has been questioned and even turned on its head by modern technologies.

By combining biometrics with automated ID verification, not only is security enhanced through the use of sophisticated machine learning techniques to identify fraud, but the customer can now save a trip to the bank, does not have to stand in a long line, and can do all of these steps from the comfort of their own home. Small things like collecting the customer’s personal data from their ID to prefill the rest of their application will save them time and pain, resulting in higher satisfaction.

Cost

According to the paper on the cost involved in compliance, new EU Anti-Money Laundering and Counter-Terrorist Financing legislation have increased the cost of non-compliance fines in the United States to around four million dollars per bank per year. Since companies can also incur reputational harm, and in certain situations the loss of a licence to operate or personal culpability among top management in addition to penalties and fraud losses.

By tapping into digital channels, a financial institution (FI) not only may contact more consumers but the prices of a procedure that AI can accomplish for them automatically would be drastically lowered. All of this saves time and money for everyone while increasing security and compliance, all while improving the customer experience and the FI’s competitiveness in a rapidly changing business.

What are the ingredients needed for an effective onboarding process?

Customer requirements in banking are changing as new generations enter the market. These clients are looking for ease and quickness. They are less interested in developing personal connections for ordinary banking goods and services, and they have less time in their schedules to do so in person.

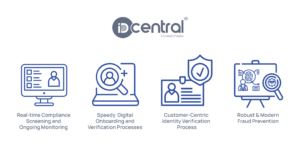

Compliance should always come first

The remainder of the advantages is meaningless unless you first “tick off” the regulatory compliance box. Understanding regulatory regulations like GDPR, anti-money laundering, and terrorist financing legislation is an important part of your client identity verification process inside your onboarding procedure.

Speed

A lengthy customer onboarding process is no longer acceptable in today’s world, but thankfully, the correct solutions may significantly improve the situation. Employing a series of tailored onboarding steps based on our expertise in the field is the base rule to get started. These predefined flows include the essential methods for gathering and storing all of the data required to fulfil those regulatory criteria.

These flows employ tools such as AI-powered Face Match and ID Verification to determine the true identity of the individual in question, as well as tools such as optical character recognition to automatically extract data from a validated identity document in order to perform over 20,000 global data checks such as sanctions lists, politically exposed individuals, negative media, and so on.

A user-friendly interface

As with any digital platform, the user interface is critical since it engages your customers(both current and prospective) and has a significant influence on retention. The simplicity of use of a banking or fintech onboarding programme is critical, and a clear, step-by-step path takes consumers towards the goals that you’ve set for them.

A Robust & Modern Identity Verification system

It goes without saying that the best, user-friendly onboarding platform is useless without an robust identity verification system to authenticate the customer. A modern Identity Verification system allows for more secure identity verifications and assessments of all acquired identification and compliance data like IDs, including facial photographs, document images, watchlist findings, and more.

What are the Best Practices in Digital Client Onboarding

In recent years, it’s fair to say that FinTechs have posed a serious threat to conventional banks in terms of client onboarding, particularly when it comes to delivering loans rapidly or remotely opening an account.

Using internet platforms: Lenders in India now have allowed near-real-time loan disbursement through a completely digital approach.

According to industry experts adaptation of online platforms has been one of the most important accelerators for fintechs to attain lightning-fast speed. In a peer-to-peer (P2P) lending paradigm, for example, the internet platform provides a standardised loan application procedure and facilitates direct matching and transactions between borrowers and lenders. People requesting loans enter financial details, and lenders analyse their demands on the site, rapidly satisfying both parties.

Adapting your onboarding procedures to your target audience

Most fintechs are now gaining market share by focusing on specific customer segments and developing individualised goods and services for these demographics and offerings. There are FinTechs that are specially tailored services to student loans and offer a whole onboarding experience geared for young people, using social media and employing cutting-edge collaborative approaches.

Data and analytics are well-established

FinTechs have mastered data and analytics, and they have smartly developed shared data linkages with banks to speed up the user verification process while keeping client credentials safe. They also employ a large number of touchpoints with clients to track incomings and outgoings and make educated guesses about how likely a certain consumer is to repay a loan, for example. According to industry experts, several FinTechs have integrated data from UPS, Amazon, QuickBooks, Yodlee, Yelp, Facebook, LinkedIn, and a variety of other sources into their systems for analytical reasons.

Artificial Intelligence

In addition to conventional analytics, fintechs are increasingly employing machine learning and other artificial intelligence modelling approaches. PayPal, for example, has decreased erroneous fraud attempts by 50% thanks to the usage of AI-based verification solutions.

How API based Onboarding solutions work

If you have the funds and capabilities, you can consider creating a tailored onboarding programme for your specific business and clientele. You may, however, be unaware of another option.

Cloud-based onboarding solutions like the IDcentral’s Onboarding platform can be readily customised to the demands of various banks and FinTechs: Through the account management panel, any financial institution may easily select from a range of preset authentication flows, such as KYC/AML for Financial Services, or design a bespoke flow with stages tailored to its business, industry, or regulatory requirements.

Finally, IDcentral’s Rest APIs make it a breeze to integrate the new authentication flow into your website and/or mobile application. Each flow, and there may be endless flows based on client categories, services or goods, customer locations, or even whatever stage of the customer journey they’re at, will then feed back into the central account management console where the success or failure of each customer is recorded.

Why cloud-based onboarding solutions provide better customer experience

With a rising number of transactions shifting to digital channels, aided by smart devices, and worldwide events like the COVID-19 epidemic, being able to safely and precisely verify identities is more crucial than ever. At the same time, banks and FinTech businesses must remember to balance security and user experience to ensure that both compliance and customer satisfaction needs are satisfied. If you’re searching for a low-cost option for establishing this journey, consider solutions like IDcentral’s Identity verification, which can be customised according to the needed thresholds and adapted to your specific needs.

Try IDcentral’s KYC – AML Screening solution with AI-based Document Verification

Sumanth Kumar is a Marketing Associate at IDcentral. With hands-on experience with all of IDcentral’s KYC and Onboarding Technology, he loves to create indispensable digital content about the trends in User Onboarding across multiple industries.

Aadhaar Plus

Aadhaar Plus  Document Verification

Document Verification  Liveness Detection

Liveness Detection  Face Trace

Face Trace Face Match

Face Match  Government DB Check

Government DB Check  Video KYC

Video KYC  Hover Plus

Hover Plus  DeepScan

DeepScan  Identity Verification

Identity Verification AML Screening & Monitoring

AML Screening & Monitoring  Digital Onboarding

Digital Onboarding  KYX Solution

KYX Solution  Banking and Financial Services

Banking and Financial Services Telecommunication

Telecommunication  Insurance

Insurance  Gaming

Gaming Retail Services

Retail Services  Shared Economy

Shared Economy Travel

Travel  Blog

Blog Webinars

Webinars Whitepapers

Whitepapers Infographics

Infographics Identity Dictionary

Identity Dictionary Frequently Asked Questions

Frequently Asked Questions